As we note in our major study on provincial gambling policy in Canada,1 gambling profits function as a hidden and regressive tax that disproportionately burdens the poor and the addicted. Households in Canada’s lowest income quintile spend an average of 5.7 percent of their income on gambling each year, nearly three times the rate paid by the country’s highest-quintile households. Meanwhile, between 15 and 50 percent of gambling revenue comes from problem gamblers, even though they make up only 1–4 percent of the population. If government is to continue deriving revenues in this manner, how could gambling money be put to better use? How might government build a gambling structure that empowers those on the economic margins, rather than preying on them?

The harmful way in which gambling profits are collected means that these funds should be kept separate from tax revenue. Ontario’s government should properly account for its reliance on these hidden taxes. Moving gambling revenue out of the consolidated fund and into a specific fund would be the equivalent of the government admitting it has a problem, admitting that it has harmed the public it is intended to protect, and forming the first steps to making direct amends.

The best way for it to make amends is to take these funds and direct them toward policies aimed at addressing the savings gap. It is much more difficult for poorer Canadians to save and build assets than it is for their middle- and upper-class counterparts, not only because of their lower incomes but also because government incentives to save are tailored to higher earners. Yet even a small amount of savings can reduce financial vulnerability significantly, especially for those who lack access to good credit. Putting a few hundred dollars away in a rainy-day fund creates a buffer against economic hardship and reduces the risk of turning to expensive, predatory options like payday loans when faced with a cash crunch. Every year, meanwhile, casinos and lotteries siphon these spare dollars out of families’ bank accounts and into governments’ pockets. Restructuring Ontario’s gambling system to ensure that funds are used to incentivize savings for those on the economic margins would rectify the injustice inherent in our current system and further the prospects of Ontario’s poor.

Building financial security for all Canadians, but especially for the most vulnerable, is widely recognized as an important policy priority. With public budgets already upended by the pandemic, governments have a unique opportunity to kick their gambling addiction with relatively little disruption to provincial balance sheets. It’s time to reform the provinces’ gambling scheme to work for, not against, low-income households. But how? We examine four options below.

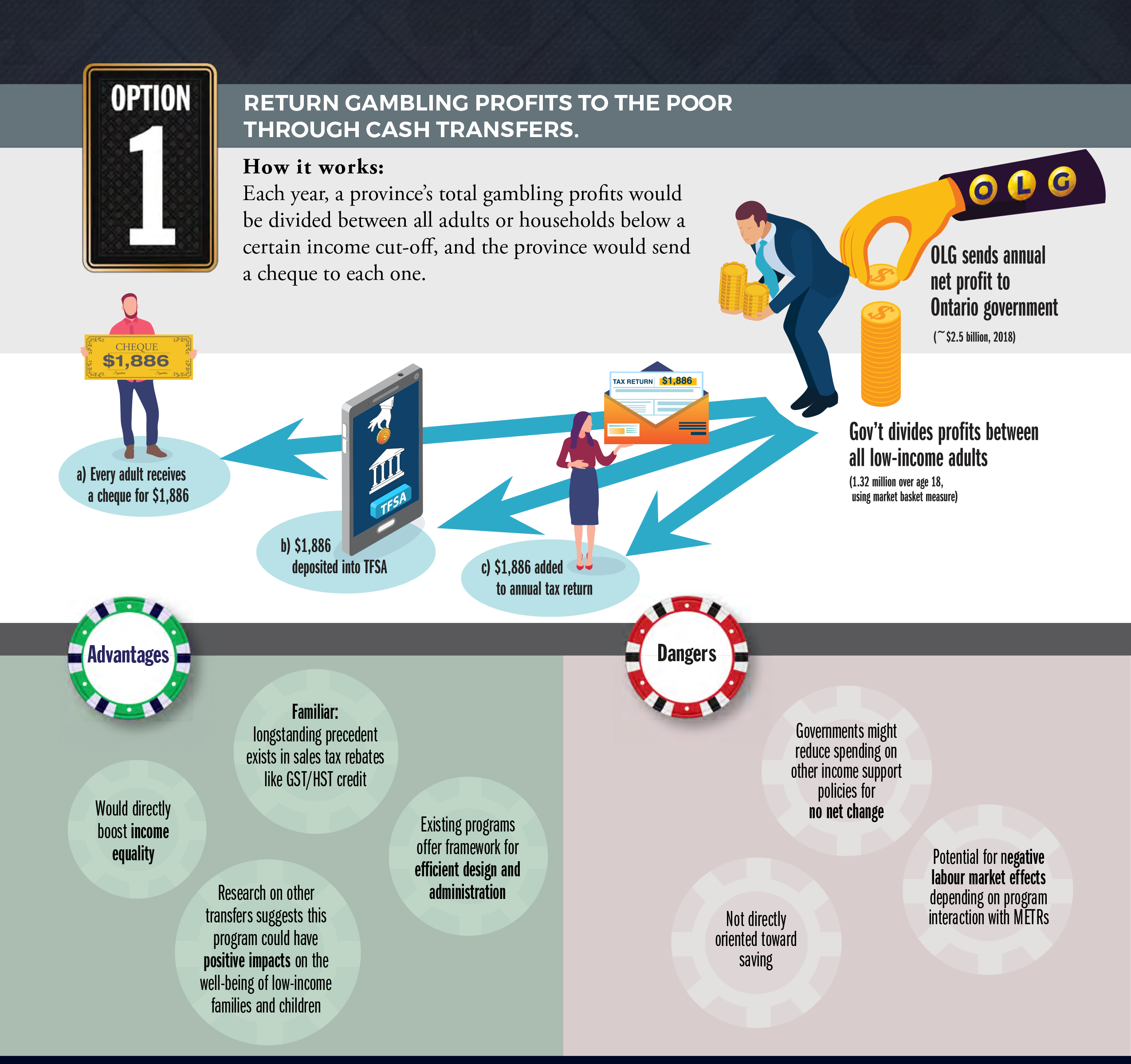

Option 1: Return gambling profits to the poor through cash transfers

How it works

Each year, a province’s total gambling profits is divided among all adults or households below a certain income cut-off, and the province sends a cheque to each one.

Advantages

- Familiar: longstanding precedent exists in sales tax rebates like GST/HST credit

- Existing programs offer a framework for efficient design and administration

- Would directly boost income equality

- Research on other transfers suggests this program could have positive impact on the well-being of low-income families and children

Dangers

- Governments might reduce spending on other income-support policies, for no net change

- Potential for negative labour-market effects, depending on program interaction with METRs

- Not directly oriented toward saving

Key policy considerations

- Lump sum rather than monthly payment encourages saving the benefit rather than treating it as income supplement

- Depositing payment in recipient’s TFSA would nudge toward saving

- Consider partnering with civil-society organizations to offer tax-time saving incentive

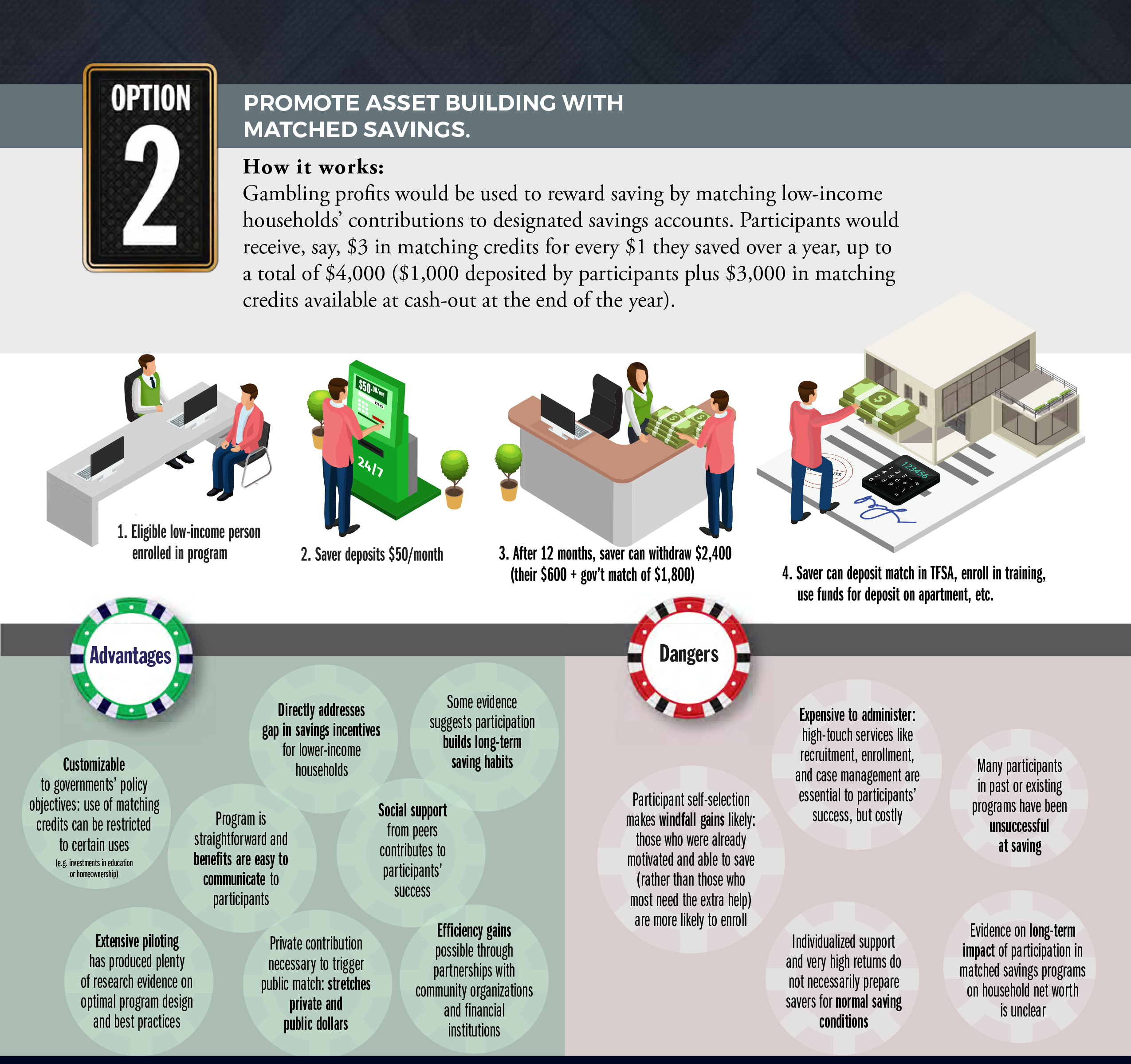

Option 2: Promote asset building with matched savings

How it works

Gambling profits are used to reward saving by matching low-income households’ contributions to designated savings accounts. Participants would receive, say, $3 in matching credits for every $1 they saved over a year, up to a total of $4,000 ($1,000 deposited by participants plus $3,000 in matching credits available at cash-out at the end of the year).

Advantages

- Directly addresses gap in savings incentives for lower-income households

- Customizable to governments’ policy objectives: matching credits can be restricted to certain uses (e.g., investments in education or homeownership)

- Program is straightforward and benefits are easy to communicate to participants

- Some evidence suggests participation builds long-term saving habits

- Extensive piloting has produced plenty of research evidence on optimal program design and best practices

- Social support from peers contributes to participants’ success

- Private contribution necessary to trigger public match: stretches private and public dollars

- Efficiency gains are possible through partnerships with community organizations and financial institutions

Dangers

- Expensive to administer: high-touch services like recruitment, enrollment, and case management are essential to participants’ success, but costly

- Participant self-selection makes windfall gains likely: those who are already motivated and able to save (rather than those who most need the extra help) are more likely to enroll

- Many participants in past or existing programs have been unsuccessful at saving

- Individualized support and very high returns do not necessarily prepare savers for normal saving conditions

- Evidence on long-term impact of participation in matched-savings programs on household net worth is unclear

Key policy considerations

- Important to ensure saving will not trigger asset limits on other means-tested programs: saving should not jeopardize participants’ existing benefits

- Participants should have some flexibility to withdraw funds in case of an emergency

- Financial-management training should be tailored to participants’ needs if included, but may not be necessary: lower-income households are often highly skilled at financial management

- Partnerships with community organizations are essential to reach target population

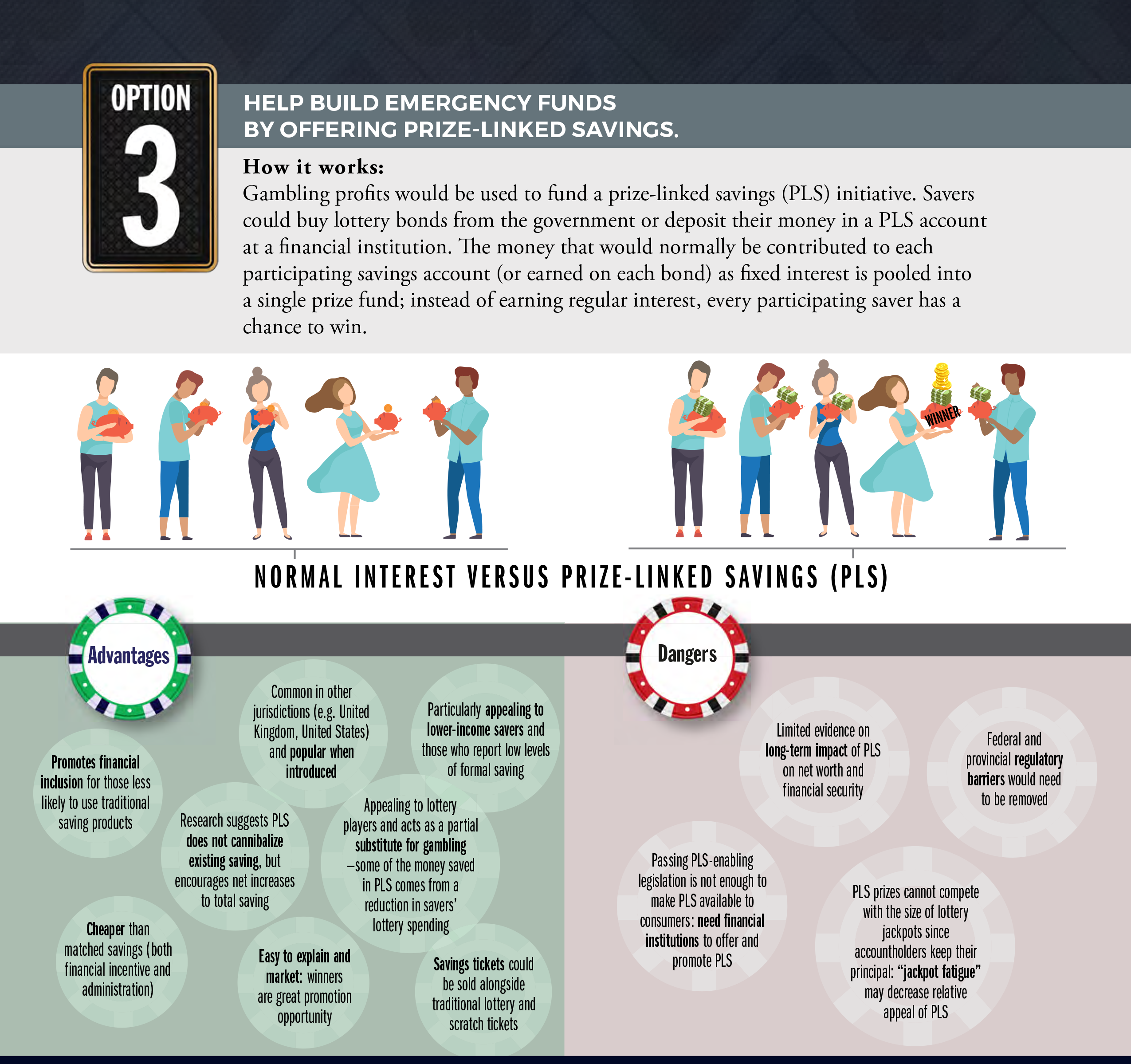

Option 3: Help build emergency funds by offering prize-linked savings

How it works

Gambling profits are used to fund a prize-linked savings (PLS) initiative. Savers buy lottery bonds from the government or deposit their money in a PLS account at a financial institution. The money that would normally be contributed to each participating savings account (or earned on each bond) as fixed interest is pooled into a single prize fund; instead of earning regular interest, every participating saver has a chance to win.

Advantages

- Common in other jurisdictions (e.g., United Kingdom, United States) and popular when introduced

- Particularly appealing to lower-income savers and those who report low levels of formal saving

- Promotes financial inclusion for those less likely to use traditional saving products

- Research suggests PLS does not cannibalize existing saving but encourages net increases to total saving

- Appealing to lottery players and acts as a partial substitute for gambling; some of the money saved in PLS comes from a reduction in savers’ lottery spending

- Cheaper than matched savings (both financial incentive and administration)

- Easy to explain and market: winners are great promotion opportunity

- Savings tickets could be sold alongside traditional lottery and scratch tickets

Dangers

- Limited evidence on long-term impact of PLS on net worth and financial security

- Federal and provincial regulatory barriers would need to be removed

- Passing PLS-enabling legislation is not enough to make PLS available to consumers: need financial institutions to offer and promote PLS

- PLS prizes cannot compete with the size of lottery jackpots, since accountholders keep their principal: “jackpot fatigue” may decrease relative appeal of PLS

Key policy considerations

- Need to make PLS products easily accessible by offering them where potential customers currently buy lottery tickets and do their banking (e.g., convenience stores, grocery stores, online), which requires partnering with lottery-ticket retailers

- PLS is better suited to modest-sized, medium-term emergency funds than to large, long-term investments like retirement savings

- Important to offer both large jackpots and smaller, more frequent prizes to prevent program fatigue

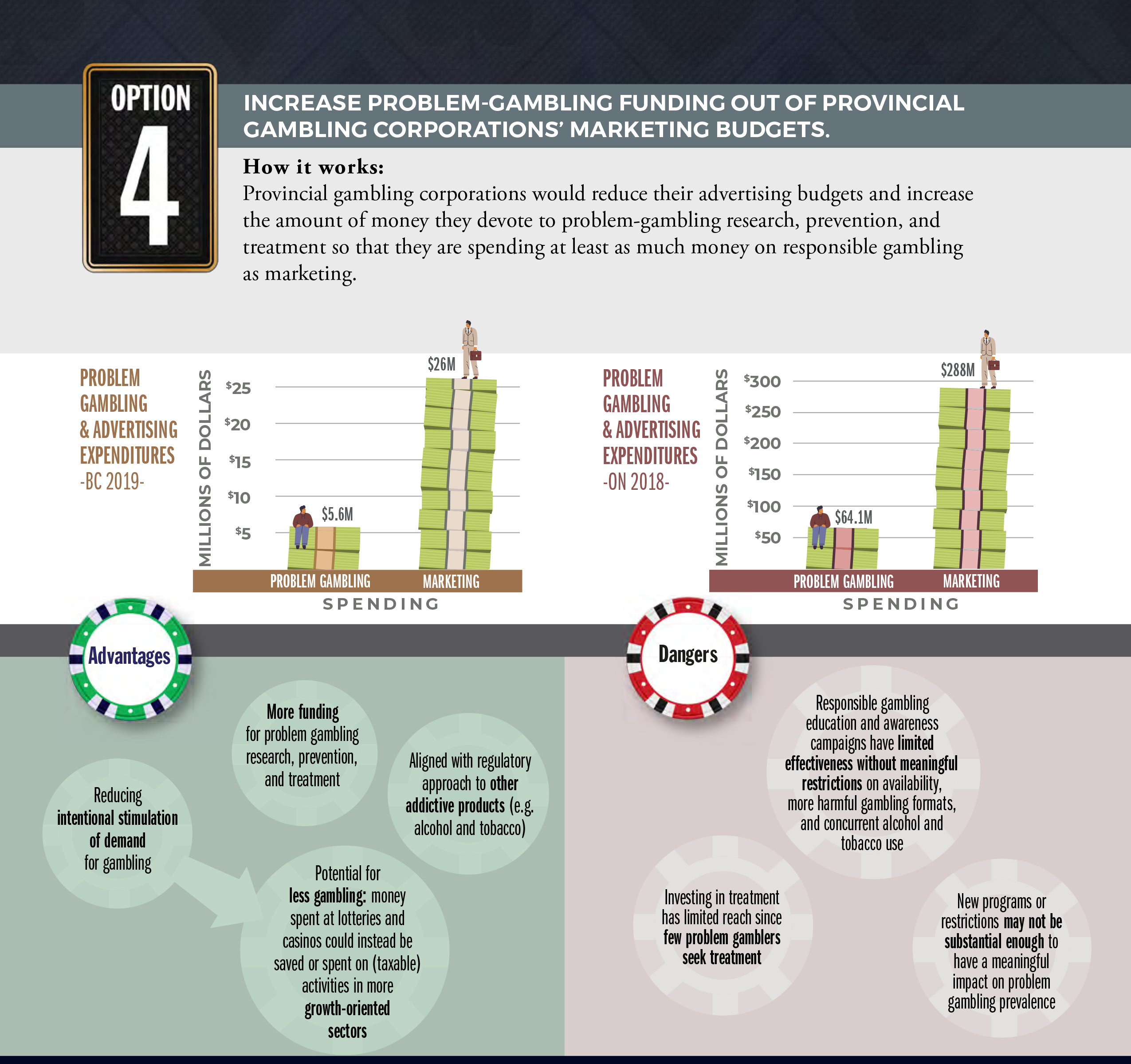

Option 4: Increase problem-gambling funding out of provincial gambling corporations’ marketing budgets

How it works

Provincial gambling corporations reduce their advertising budgets and increase the amount of money they devote to problem-gambling research, prevention, and treatment, so that they spend at least as much money on responsible gambling as on marketing.

Advantages

- More funding for problem-gambling research, prevention, and treatment

- Aligned with regulatory approach to other addictive products (e.g., alcohol and tobacco)

- Reduces intentional stimulation of demand for gambling

- Potential for less gambling: money spent at lotteries and casinos could instead be saved or spent on (taxable) activities in more growth-oriented sectors

Dangers

- Responsible-gambling education and awareness campaigns have limited effectiveness without meaningful restrictions on availability, more harmful gambling formats, and concurrent alcohol and tobacco use

- Investing in treatment has limited reach, since few problem gamblers seek treatment

- New programs or restrictions may not be substantial enough to have a meaningful impact on problem-gambling prevalence

Key policy considerations

- 26 percent of Canadians have a personal connection to problem gambling: these Canadians are more likely to view gambling as harmful and have a negative view of government involvement in gambling

- EGMs are among the most harmful gambling formats and have been linked to problem gambling but provide significant revenue to bars and pubs: cooperation is required to reduce the reach of EGMs and protect owners’ businesses

- Since problem gamblers contribute disproportionately to provinces’ gambling revenue, an effective policy change will necessarily involve a reduction in revenue